Food Deflation And Why It Hurts The Grocery Industry

Summary

Food prices are in a deflationary environment.

Deflationary food prices put pressure on net margins and Same Store Sales.

The entry of Amazon into the grocery channel will continue to pressure margins in the industry.

Other than perhaps Walmart, the industry remains a risky investment.

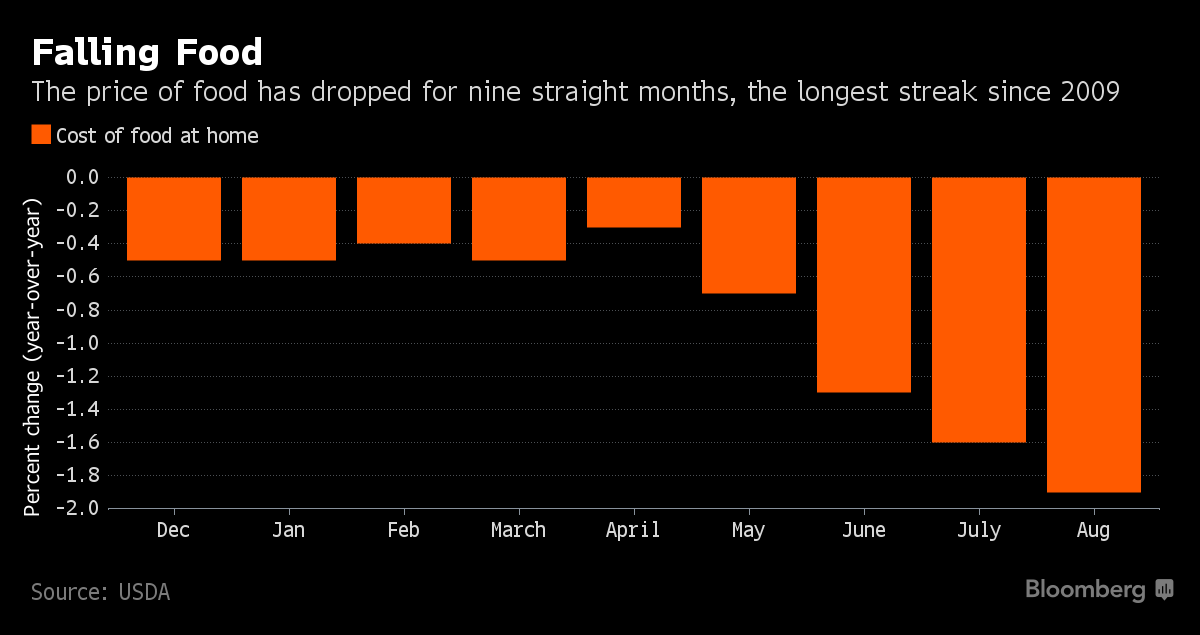

Prices of Food products and groceries in general have been in an unprecedented deflationary environment since 2015. Commented Rupesh Parikh, senior analyst at Oppenheimer:

The current food deflation cycle has lasted much longer than most anticipated, with the latest data point representing the worst reading.Based on our work, we see the possibility of food deflation persisting well into next year, potentially through the middle of 2017. As a result, we continue to believe shorter-term investors should steer clear of grocery names.

Below is a chart from Bloomberg showing the deflationary spiral of food and grocery as it progressed through 2016.

Source USDA via Bloomberg

Source USDA via Bloomberg

Currently in 2017, through May, the 12 month adjusted average per the United States Department of Labor and Statistics is negative for "Food at Home" at minus .2%.

Real world examples from Costco (NASDAQ:COST) on their price slashing:

Costco has cut some of its food prices as much as half. A carton of 18 extra large eggs was $3.61 last year. It came down to $1.79. A three-pound bag of Kirkland Signature pistachios was $19.99. It fell to $14.99; Arm & Hammer liquid laundry detergent came down to $10.99 from $15.79.

Source: USA TODAY

In 2014 and 2015, Meat, chicken and eggs saw the biggest cuts because of oversupply and lower than expected exports. According to the USDA, agricultural exports dropped by $17 billion or approximately 11%.

Normally, one would think that if the raw cost of the product a company is selling is in decline, that should be good for the company selling that product. For a given sales price, a lower cost would increase gross margins. But in the strange world of hypercompetitive grocery, that is not the case. There are a few reasons for this.

- The first is the speed at which deflationary pressures affect the company. The food business turns inventory rapidly. This means all the grocery chains are replenishing their stock with the same price deflated goods. Kroger (NYSE:KR), Walmart (NYSE:WMT), Publix (OTC:PUSH) etc. must all decide at what new price to sell their goods. They generally will use a fixed formula markup for their gross margin percentage – why? Because of point number 2.

- Much like the gasoline business, if one company maintains its pricing high, it doesn’t take long for the customer to figure out that they should shop at another location. In a world of so many choices, companies simply must pass these lower costs onto the consumer to keep their traffic high and not lose precious customer loyalty to others.

- With a set gross margin, the actual dollars of profit and revenue numbers decline with food deflation. However, a company’s fixed costs do not decline. They can’t lower their employees hourly pay, nor their rents, power, and marketing expenses in the same deflationary manner.

Here is an example. Let’s say Kroger buys a food item for $10 and marks the product up 30% to $13. Kroger makes $3 in gross profit, and is in line with other grocery stores in the area. But over time, the cost of the item lowers to $8. Now marking the product up the same 30% results in a sales price of $10.40. Kroger’s gross profit on the item is now $2.40. For the same volume of goods sold on this item, Kroger makes 20% less profit ($2.40 instead of $3.00) and has a corresponding revenue decline of 20% as well ($10.40 instead of $13). But their fixed costs either stay the same or continue to slowly rise.

Generally due to elasticity of demand, the demand for a given product will rise as it moves down along the price curve. Food, however, has a low elasticity of demand compared to say, luxury yachts. A family will buy a dozen eggs to meet their needs and will not suddenly buy fourteen eggs when the price drops x%. They will simply take their food savings and use it purchase more discretionary items – like flat screen TV’s.

This has two effects. The first is that Same Store Sales, or Comparable sales, begin to decline. The second is that a company’s net margin, after fixed costs, begins to decline.

Let’s examine the first - Same Store Sales. When investors examine retail stocks, Same Store Sales is a key metric – if not THE key metric. It is a snapshot of how well a store, or set of stores, is doing over time. Did the same locations make more revenue year over year? It removes the sales growth from just opening more stores and it is an indicator of the underlying health of the business concept. Investors like companies that have locations that are rising in sales year over year. This is a key figure when gauging a regional to national investment theme. I wrote another article on the topic of Same Store Sales here.

The second effect is more straightforward and simple to understand. A company with net margins declining is simply less profitable on nearly every metric – return on capital, earnings per share, earnings per square foot etc.

As we can see, food deflation can be negative for grocery store chains like Kroger, Ingles (NASDAQ:IMKTA), and Weis (NYSE:WMK) or companies that depend largely on grocery, like Wal-Mart (WMT) and Target (NYSE:TGT).

Food deflation in beef, pork, and poultry are expected to decline as much as 7% in 2017 – source FORBES. These effects have already been felt on companies like Kroger – which reported a rather disastrous Q1 report. Also, Target’s Same Store Sales continue to be negative directly due to lower grocery sales.

The effect has been felt across the grocery industry.

TGT data by YCharts

TGT data by YCharts KR data by YCharts

KR data by YCharts SVU data by YCharts

SVU data by YCharts WMK data by YCharts

WMK data by YCharts

Amazon (NASDAQ:AMZN) – The Great Deflator

Then there’s Amazon, which has caused the disruption of the status quo in so many businesses. With the proposed acquisition of Whole Foods (NASDAQ:WFM), Amazon has turned its gaze towards the food delivery and grocery business. Amazon has struggled over the years establishing a presence in grocery, but is diving in with the purchase of Whole Foods.

Amazon is the great deflator. It attacks pricing and cannot be positive to the overall supply/demand situation of the grocery industry. Already seeing price deflation, the grocery industry can expect even more competition and price pressure. This clearly has investors spooked based on the large drops in stock prices when the deal was announced. Food was long thought to be resistant to the dangers of online. Now each of these retailers will need a specific “Amazon strategy” and that defines how they will compete with the king of online retail. Any grocery retailer without such a strategy will simply not be investable. As Amazon continues to grow into the grocery business, the pure grocery chains have many years of difficulty and price pressure in front of them.

Same store sales of selected retailers.

Retailer

|

Same Store Sales (latest QTR)

|

Ingles

| |

Target

| |

Kroger

| |

Super Value

| |

Weis

|

-.9%*

|

Walmart

|

* Excludes Fuel

As you can see, Walmart has far outperformed its peers on a Same Store Sales metric. They seem to have the size and scale to compete effectively. They are the only company on the list with a positive Same Store Sales number. Here is the chart of Walmart.

WMT data by YCharts

WMT data by YCharts

Other than perhaps Walmart, none of grocery stocks are a particularly attractive investment. Walmart is well positioned for a food deflation environment. Any money saved by their customers, is likely spent on the more discretionary items in their store (i.e. the flat screen TV’s). This can help keep their Same Store Sales positive. It can be argued that Amazon’s purchase of Whole Foods validates the Walmart strategy and the value of physical retail space. Perhaps Amazon is actually playing catch up with Walmart?

The other grocery chains have strong headwinds in place in the form of food deflation and oncoming competition from Amazon. Target has struggled to try to compete with Walmart in the food space, but so far, they have not figured out a proper strategy. It may be best for them to reduce their sales on food as I opined here.

I will leave it to the value investors to decide when these stocks have fallen too far, but I would avoid the sector entirely until their Same Store Sales numbers turn positive. With Amazon entering the space, gross margins and pricing will continue to be pressured. Watch for upticks in food prices and a weakening U.S. dollar to change the current deflationary trend. Until then, we can expect more pain in the grocery space.

No comments:

Post a Comment