Costco Wholesale: A World-Class Retailer And Superb Dividend Growth Stock

Simply Safe Dividends

Follow(6,105 followers)

Dividend investing, dividend growth investing, long-term horizon, research analyst

Costco Wholesale (NASDAQ:COST) has proven itself one of the best dividend growth stocks of the last two decades, nearly doubling the S&P 500's annualized return.

However, now with founder James Sinegal retired from the CEO position (he remains on the board) and the rise of major disruptive rivals such as Amazon (NASDAQ:AMZN), the company's business model faces potential threats from numerous directions.

Let's take a look at what allowed Costco to become the juggernaut it is today, but more importantly see whether or not the granddaddy of wholesale warehouse retail deserves a spot in a diversified dividend portfolio such as our Top 20 Dividend Stocks portfolio.

Investors should note that Costco is held in Berkshire Hathaway's portfolio, and you can see analysis on all of Warren Buffett's top dividend stocks here.

Business Description

Founded in 1976 in Issaquah, Washington, Costco pioneered the wholesale warehouse retail business model and today operates 723 locations in nine countries on four continents.

While Costco is the world's second-largest retailer by sales (behind Wal-Mart (NYSE:WMT)), it generates the majority of its profits (70%) from its annual $55 and $110 executive membership fees. The company has built up a base of 87.3 million cardholders around the world.

Costco is one of the world's largest sellers of groceries, alcohol, diamonds, electronics, prescription drugs, tires, gasoline and even travel services.

While the company is working hard to expand overseas, the vast majority of sales and operating profits continue to come from its core U.S. operations.

| Business Unit | Q1 2017 Sales | Q1 2017 Operating Income | % of Sales | % of Operating Income |

| U.S. | $20.4 billion | $506 million | 72.5% | 59.6% |

| Canada | $4.1 billion | $191 million | 14.6% | 22.5% |

| Other International | $3.6 billion | $152 million | 12.9% | 17.9% |

| Total | $28.1 billion | $849 million | 100.0% | 100.0% |

Source: Costco Fiscal Q1 2017 10-Q

Business Analysis

Unlike most brick-and-mortar retailers, Costco's business model is built around a wide moat, courtesy of its extremely loyal customer base (88% annual global renewal rate). Specifically, the company's membership fees allow it to offer consumers greater discounts on both name brand and its own store brand goods.

In addition, the company is legendary for low turnover in its workforce, courtesy of much higher than average pay and benefits. This also helps to maintain strong brand equity thanks to employees that are happier and offer superior customer service compared to most of its rivals.

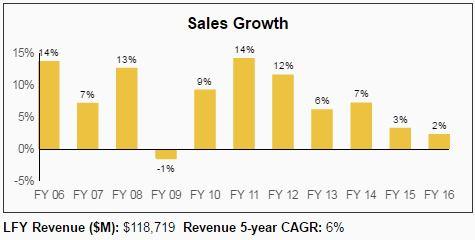

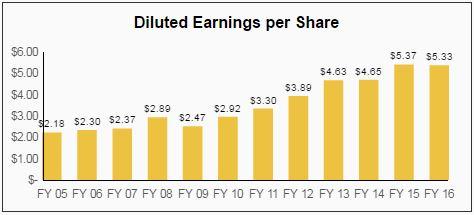

The combination of excellent service and reasonable prices has helped Costco gain and maintain its strong market share in its home U.S. market. However, in recent years saturation of the U.S. market has resulted in slowing sales and earnings growth.

Source: Simply Safe Dividends

Source: Simply Safe Dividends

That's especially true given that the company has increased its investments into expanding store count, especially overseas (Canada, UK, Australia, Taiwan, and South Korea), where consumer taste has indicated that the warehouse wholesale retail business model may become increasingly popular.

Management has indeed done a good job in executing on this overseas growth, with constant currency, ex-fuel same store sales (i.e. comps) growing nicely in both Canada and overseas.

Source: Costco Fiscal Q1 Earnings Release

In fact, in the most recent conference call, CFO Richard Galanti announced that the company plans to open 31 new stores in 2017, up from 29 in 2016.

While a 4.3% increase in global store count won't necessarily return Costco to its former glory days of double-digit sales growth, it should help double revenue growth (to 5% to 7%) compared to last year if comps stay the same or improve just slightly (1% to 3%).

Numerous Wall Street analysts have criticized Costco for years about its subpar margins, which are courtesy of its company policy of paying employees far above industry standards in both pay and benefits.

| Company | Operating Margin | Net Margin | FCF Margin | Return On Assets | Return On Equity | Return On Invested Capital |

| Costco | 3.1% | 2.0% | 2.2% | 6.7% | 21.2% | 14.5% |

| Industry Average | 5.0% | 3.1% | NA | 7.1% | 19.8% | NA |

Source: Morningstar

For example, Costco just announced an increase in its minimum wage from $13.00 per hour to $13.50. However, due to very low turnover, most of its starting employees last the four years it takes to reach the company's top wage rate of $22.50.

That's about double the wage earned by most U.S. retail employers, which is about $11.50. In addition to high pay, nearly 90% of employees also receive company-provided health insurance and a pension plan.

While this unique style of "socially responsible" capitalism is relatively new to the U.S., studies actually show that it is a vital part of Costco's special sauce.

For example, according to MIT Sloan School of Management Professor Zeynep Ton, longer tenured workers who are happier, feel more appreciated and less worried about making ends meet make for a far better customer experience.

"How many times have you gone to a store, and the shelves are empty or the checkout line is too long, or employees are rude? At Costco, you see a huge line that disappears in minutes."

And indeed it does appear that Costco's "treat employees well" policy is working, with sales per employee nearly double that of Wal-Mart's competing Sam's Club warehouse stores and resulting in high and consistently growing returns on capital.

In other words, from Costco's perspective, paying employees well in order to retain them for the long term just makes good business sense. And as you can see above, while Costco's operating margin may be low, it's gradually improving over time.

This is courtesy of the company's laser-like focus on efficiency. For example, unlike the average rival store, where around 60,000 items are sold, the average Costco sells just 3,700 goods.

However, thanks to its enormous sales volumes, as well as buying direct from manufacturers, Costco is able to obtain excellent wholesale prices along the lines of Wal-Mart and Kroger (NYSE:KR).

Thanks to goods being shipped directly from suppliers to stores (instead of central distribution centers), Costco is able to achieve amazing turnover that resulted in an average of $162 million in sales per store last year, 80% more than the $90 million per store achieved at Sam's Club.

In fact, the $1,100 per square foot in annual sales achieved at Costco is truly astonishing, and generally only seen at luxury retailers or high-end jewelry stores.

Given that this figure is double and triple that of Sam's Club and Wal-Mart ($680 and $400 per square foot, respectively, according to Morningstar), it appears that Costco's unique business model is firing on all cylinders.

This is especially true given the rise of online retail competition, which has yet to harm its business as it has so many other retailers. Costco's strategy of selling numerous loss leaders, such as groceries and gas, to attract customers and make up for it with higher margin goods, has helped to insulate the retailer from the threat of Amazon.

In fact, Costco's own online platform is seeing good results, with online sales up 8% in the most recent quarter, far better than the company's 3% overall sales growth.

Overall, Costco is a competitively advantaged firm thanks to its economies of scale, intentionally limited product selection, quality in-store experience, and loyal base of shoppers who provide high-margin, recurring membership fee revenue.

While Costco's best days of domestic growth are likely over, it is still a wonderful business that should be around for decades to come.

Key Risks

While Costco's consistent growth over time has certainly benefited long-term investors and the company has shown an exemplary dedication to growing its dividend, there are certain important risks to keep in mind.

First, remember that Costco's earnings growth thesis is largely predicated on continued growth of its membership base, especially upgrading as many people as possible to its executive level. That strategy is predicated on consumers continuing to value their membership, largely for the perceived long-term cost savings.

However, despite its low prices, cost savings aren't guaranteed. According to organizational psychologist Billie Blaire, "membership fees, wastage from overbuying (produce and such), the necessity to buy in quantity (canned goods that sit on shelves and have to be discarded), etc." can actually mean that cost savings are mostly illusionary.

Given the executive membership's much higher annual fee, the retention rate for that level is only 40%. In addition, as Costco expands more overseas it is counting on consumers in other countries finding the bulk warehouse shopping experience convenient enough to choose it over alternatives such as Amazon's Prime Now online service, which offer 1-2 hour delivery in certain markets.

Costco investors are essentially betting that, in the long term, the suburban-based (it's hard to build giant warehouses in urban areas), buy-in-bulk shopping model will remain popular not just with U.S. customers but also those in more crowded nations such as in Europe and Asia.

If this assumption proves to be incorrect, Costco's long-term growth rate will almost certainly disappoint investors and cause the stock to underperform (more on COST's current expectations later).

Online retail could also pose a threat to the company's long-term growth. While Costco is working towards strengthening its online presence to maintain market share, keep in mind that its warehouse and bulk good focused business model is less online-friendly than rivals such as Wal-Mart and Target (NYSE:TGT).

For example, Costco's 8% growth in online sales is a pale shadow of the 21% and 26% online sales growth experienced in the most recent quarter at Wal-Mart and Target, respectively.

Finally, we can't forget the fact that as Costco diversifies overseas it faces ever higher currency risks. Right now the stronger dollar, a result of superior economic growth in the U.S. and rising interest rates, means that much of the comp growth from overseas is being negated.

Expanding international operations also pose operational risks and could weigh on overall company profitability until they scale up to maturity.

Dividend Safety Analysis: Costco

We analyze 25+ years of dividend data and 10+ years of fundamental data to understand the safety and growth prospects of a dividend.

Our Dividend Safety Score answers the question, "Is the current dividend payment safe?" We look at some of the most important financial factors such as current and historical EPS and FCF payout ratios, debt levels, free cash flow generation, industry cyclicality, ROIC trends and more.

Dividend Safety Scores range from 0 to 100 and conservative dividend investors should stick with firms that score at least 60. Since tracking the data, companies cutting their dividends had an average Dividend Safety Score below 20 at the time of their dividend reduction announcements.

We wrote a detailed analysis reviewing how Dividend Safety Scores are calculated, what their real-time track record has been, and how to use them for your portfolio here.

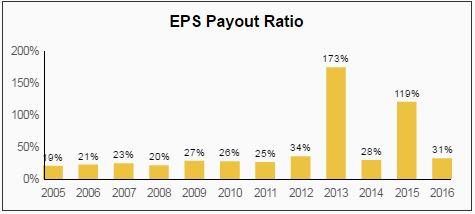

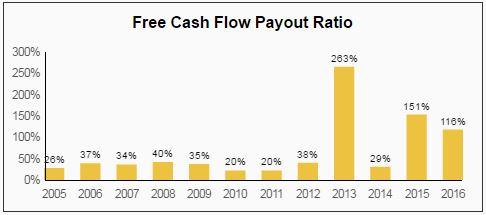

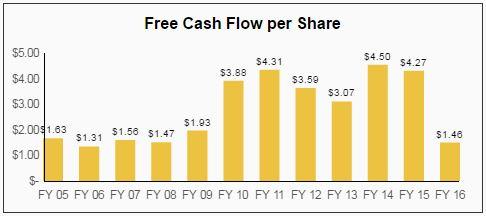

Costco has a Dividend Safety Score of 94, indicating that its dividend is extremely safe and dependable. As you will see, Costco has a good track record of maintaining a conservative EPS and free cash flow (FCF) payout ratio, providing a high level of dividend security.

While occasionally increased growth investment causes a spike in these ratios (see below), over the long term the company's payout is very well covered by free cash flow.

In fact, over the past 12 months Costco's EPS payout ratio was just 32%, meaning that the payout is very safe and has plenty of room for future growth.

Source: Simply Safe Dividends

Source: Simply Safe Dividends

Costco's business is also recession-resistant. Company sales were down just 1% in fiscal year 2009 and free cash flow actually grew that year. The company's stock also outperformed the S&P 500 by 11% in 2008.

These defensive qualities make Costco's dividend safer and the company's consistent free cash flow generation, which is needed to sustainably pay dividends, further reduces its risk profile.

Source: Simply Safe Dividends

As importantly, Costco boasts a pristine balance sheet, courtesy of its net cash balance (i.e. more cash than debt) and exceptionally high interest coverage ratio.

Source: Simply Safe Dividends

And you can see, when compared to its peers, Costco's balance sheet appears even more impressive, with a much lower leverage ratio and lower debt/capital ratio, helping explain the company's high credit rating.

This allows the company to keep borrowing costs very low (as low as 1.75% for five-year bonds) and helps lower its overall cost of capital.

| Company | Debt / EBITDA | EBITDA / Interest | Debt / Capital | Current Ratio | S&P Credit Rating |

| Costco | 1.0 | 39.6 | 22% | 0.97 | A+ |

| Industry Average | 1.56 | NA | 38% | 0.94 | NA |

Source: Morningstar

A strong balance sheet improves Costco's financial flexibility and allows for continued growth of global store count and the dividend.

Dividend Growth Analysis

Our Dividend Growth Score answers the question, "How fast is the dividend likely to grow?" It considers many of the same fundamental factors as the Safety Score but places more weight on growth-centric metrics like sales and earnings growth and payout ratios. Scores of 50 are average, 75 or higher is very good and 25 or lower is considered weak.

Costco has a Dividend Growth Score of 81, meaning that dividend lovers can likely expect Costco's solid history of double-digit dividend growth to continue for many years to come.

Costco didn't start paying regular dividends until 2004. Since then, Costco has raised its dividend every year, proving itself dedicated to strong, consistent growth of its payout (even during the financial crisis). This gives me confidence that Costco's dividend growth prospects are relatively recession-resistant given its low payout ratio.

As seen below, Costco's dividend has consistently grown by about 13% annually over time. The company last raised its dividend by 12.5% in early 2016.

Source: Simply Safe Dividends

Currently, analysts expect Costco to open 25 to 40 stores a year, which combined with stable comps of 1-2% should allow for long-term sales growth in the mid-single digits.

Add in slowly expanding margins and a slow but steady buyback program, and Costco's EPS growth could reasonably achieve a consistent 8% to 9% in the coming years. That easily translates to double-digit dividend growth for the foreseeable future.

Just keep in mind that Costco's current yield of 1.1% means that this is a true dividend growth stock and won't be generating strong income until several decades down the road.

Valuation

Costco's superb business model and excellent growth track record mean that the company's stock generally trades at a high premium.

| P/E | 13 Year Median P/E | Yield | 13 Year Median Yield |

| 29.1 | 24.7 | 1.1% | 1.1% |

Source: Gurufocus

The current P/E multiple of 29.1 is significantly higher than COST's historic norm, indicating that Costco's shares are potentially overvalued relative to history. In fact, the P/E is near a 10-year high, indicating that investors interested in owning Costco should probably wait for a pullback before opening a position.

If you already own Costco shares, it probably makes sense to wait for a better time to add to your position, such as after a disappointing earnings announcement or the next inevitable, if unpredictable, market correction.

Closing Thoughts on Costco

Costco's unique membership-focused business model, long track record of operational excellence, and consistent dedication to strong dividend growth means that, from a fundamental perspective, it represents an excellent long-term dividend growth stock.

That being said, the current valuation is so high as to greatly increase the risk of owning this stock, at least in the short to medium term. Therefore, it's probably a good idea to add Costco to one's watchlist and wait for a more attractive buying opportunity. A stock price below $140 per share would start to get my attention (COST currently trades at $161)

No comments:

Post a Comment